The Quiet Cost of Cash

Why Playing It Too Safe Can Hurt You Long Term

By: Cole Conkling

For many investors, the allure of a risk-free 4-5% return on cash via short-term Treasury Bills feels like a no-brainer. In a world that has seen both extreme market volatility and persistent uncertainty, earning a steady yield with no drawdowns can feel like winning. And to be fair, for immediate needs, an emergency fund, or short-term goals, holding cash in T-Bills or similar instruments makes perfect sense. But here's the catch: over the long term, playing it safe can quietly erode your wealth.

The Illusion of Safety

Cash is often perceived as the most secure investment. There’s no volatility, no headline risk, no earnings reports to stress over. But what appears safe on the surface can be deceptively expensive and risky over time. Consider this: the "risk-free" rate—often defined as the yield on short-term U.S. Treasury Bills—frequently moves in tandem with inflation. This means that, in real terms, the return on cash (that is, your return after adjusting for the eroding power of inflation) is often close to zero. In financial terms, this is the distinction between “nominal” and “real” returns.

A “nominal” return is what you see on paper—say, 4% on a Treasury Bill. A “real” return is what you actually earn after inflation. If inflation is running at 4%, your real return is effectively zero. In some periods, especially during high inflation, real returns on cash can even be negative. This is why economists often refer to cash as “a melting ice cube.” It feels solid but slowly diminishes in value over time.

Put simply, the whole point of investing is to preserve and grow your purchasing power over time—i.e., to earn a sufficient real return. It’s not just about having more dollars—it's about having more buying power to put those dollars to use. If your investments aren’t outpacing inflation, then you’re not actually getting ahead. You’re just running in place (or even falling behind). And over the span of a lifetime, that can make the difference between financial independence and coming up short.

Historical Context: Cash vs. Markets

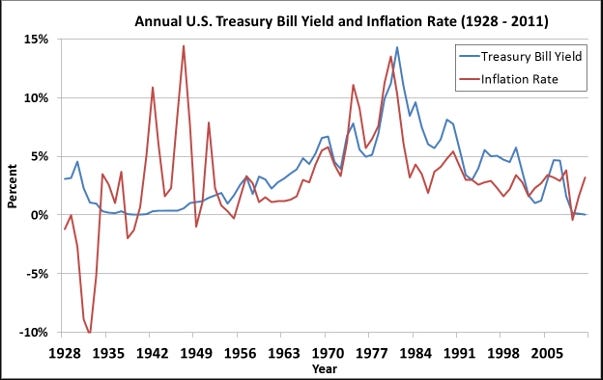

Let’s examine how this plays out historically. From 1928 to 2023, the average annual return on U.S. Treasury bills was about 3.3%—while inflation averaged approximately 3%. That’s a razor-thin real return of 0.3%. Indeed, as the chart below shows, the risk-free treasury rate and inflation are well correlated. Therefore, when inflation tracks higher, so too does the risk-free rate, brining down the real return of T-Bills and eroding the value of your cash:

During the same period, long-term government bonds returned about 5.1%, and U.S. stocks returned roughly 9.8% annually. That difference in compounded growth is massive over time. A $10,000 investment in 1928, left in Treasury bills, would have grown to just under $220,000 by 2023. The same amount invested in stocks would have grown to over $70 million!

The S&P 500’s strong performance over decades isn’t just about high returns—it’s about time in the market. Reinvested dividends and compounding returns make a massive difference. Even bonds (i.e., longer-term treasuries, and investment grade corporate), often perceived as conservative, can outpace cash and short-term treasuries substantially over time. When markets are turbulent, it’s natural to flee to safety. But history shows that doing so for extended periods almost guarantees underperformance relative to more risk on portfolios.

The Real Cost: Lost Opportunities

The hidden cost of holding too much cash is what we refer to as an opportunity cost. Every dollar sitting in cash is a dollar not compounding in an asset with higher expected returns. While the losses from stock and bond market downturns are visible and painful, the losses from missed growth are quiet and insidious.

Let’s consider a hypothetical investor who kept $100,000 in cash from 2009 to 2019. Over that decade, the S&P 500 nearly tripled in value. Meanwhile, that cash, earning near-zero returns due to historically low interest rates, barely grew at all. The difference is hundreds of thousands of dollars in lost potential.

Moreover, inflation is an invisible tax. Even when inflation is "low"—say, 2%—it still means that your money is losing purchasing power over time. At 2% inflation, the value of cash halves roughly every 36 years. At 4%, that half-life drops to just 18 years.

Behavioral Finance: Why We Favor Cash

Part of the reason investors gravitate toward cash is behavioral. Cash feels safe. It doesn’t go down in value on a screen. It doesn’t make headlines. And in uncertain times, doing nothing can feel better than doing something wrong. But what feels safe isn’t always sound. Behavioral economists call this loss aversion—our tendency to fear losses more than we value gains. This bias leads many to over-allocate to cash, especially during turbulent markets.

There’s also recency bias—the tendency to project recent trends into the future. If markets have been volatile, we assume they’ll stay volatile. If cash has yielded 4-5%, we assume it will always yield that much. But history suggests otherwise. Interest rates are cyclical. The higher cash returns we see today are unlikely to persist over the next decade.

Other biases, such as the availability heuristic, cause investors to overweight dramatic events. A sharp downturn in equities looms large in memory, while the silent erosion of purchasing power gets ignored.

Strategic Liquidity: The Role of Cash

None of this is to say cash has no place. It absolutely does. Cash is essential for emergency funds, near-term expenses, and as a cushion during market downturns. But its role should be strategic, not excessive. For example, financial planners often recommend bucketing assets by time horizon and purpose:

0–1 years: Cash and cash equivalents (immediate needs; safety net)

2–10 years: Short to intermediate-term bonds mixed with equities depending on risk tolerance (global diversified)

10+ years: Equities and growth-oriented assets (long-term, high growth bucket)

Thoughtful portfolio construction acknowledges that different assets serve different functions. Cash isn’t meant to generate wealth—it’s meant to give you stability and to ensure you don’t have to sell your riskier assets during times of market downturns or personal emergency.

The Quantor Core Strategy: Diversify, Enhance, Endure

For investors looking to move beyond cash without taking on unnecessary risk, the Quantor Core Strategy offers a compelling option. It’s built on a simple but powerful idea: diversify intelligently, enhance with leverage prudently, and endure the inevitable ups and downs.

The Core Strategy doesn’t chase returns. Instead, it seeks to optimize risk-adjusted returns by spreading exposure across asset classes—including global equities, bonds, and commodities—and using leverage to enhance return potential. This combination of diversification and smart risk management helps investors achieve superior long-term performance.

Final Thoughts: Don’t Let Comfort Cost You

Every portfolio needs a balance of safety and growth. But too often, investors lean too far into safety—especially in uncertain times—and forget that risk can wear many disguises. One of them is comfort. Over time, inflation compounds. So does missed opportunity. If your investment plan relies heavily on cash, you’re not just losing potential—you’re risking stagnation. Long-term investors should reframe risk not as temporary volatility, but as the failure to grow purchasing power over time. And that’s precisely the risk posed by excessive cash holdings.

Time is your greatest asset. The longer your horizon, the more power it has to work for you. Put it to use. Don’t let caution become a drag on your future. The real risk isn’t volatility—it’s inertia. And the best antidote to inertia is a strategy rooted in data, discipline, and long-term perspective. That’s what Quantor’s Core Strategy is designed to deliver: a path forward for those who want to grow their wealth sensibly and sustainably.

DISCLOSURES: Quantor Capital, LLC. (“Quantor”) is a Registered Investment Adviser ("RIA") with the United States Securities and Exchange Commission (“SEC”). Registration does not imply a certain level of skill or training, and the content of this communication has not been approved or verified by the SEC or by any state securities authority. The information presented is being provided strictly as a courtesy and for informational purposes only. It is not intended as an offer or solicitation to buy or sell any product or security. Be sure to first consult with a qualified financial adviser and/or tax professional before implementing any strategy discussed here. Certain sections of this communication have been written with the assistance of AI. All sources cited are believed to be reliable, but accuracy and completeness cannot be guaranteed.

Different types of investments involve varying degrees of risk, and there can be no assurance that any specific investment or strategy will be suitable or profitable for a client's portfolio. Past performance does not guarantee future investment success. All investment strategies have the potential for profit or loss. Changes in investment strategies, contributions or withdrawals, and economic conditions may materially alter the performance of your portfolio. There can be no assurances that a portfolio will match or outperform any particular benchmark. Asset allocation and diversification do not assure or guarantee better performance and cannot eliminate the risk of investment losses.